Leverkusen, Germany

March 5, 2025

- 2025 to be a pivotal year for company’s turnaround – improved performance expected from 2026 onwards

- Comprehensive plan to boost profitability at Crop Science

- Progress on strategic priorities

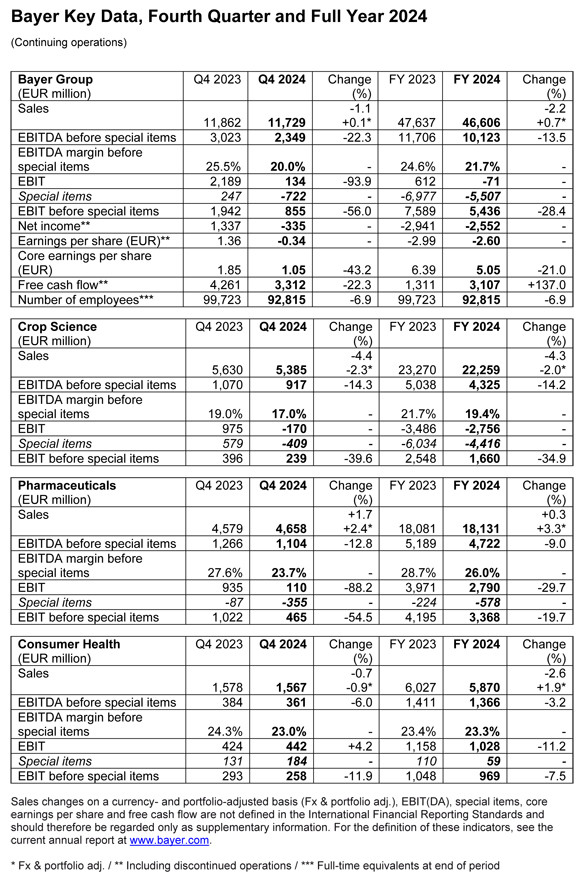

- 2024 Group sales at 46.606 billion euros (Fx & p adj. plus 0.7 percent), negative currency effects of 1.349 billion euros

- EBITDA before special items at 10.123 billion euros (minus 13.5 percent)

- Core earnings per share at 5.05 euros (minus 21.0 percent)

- Net income at minus 2.552 billion euros, impairment losses at Crop Science

- Free cash flow increases to 3.107 billion euros, net financial debt reduced to 32.626 billion euros

- Proposed dividend of 0.11 euros per share

- Outlook for 2025: Sales roughly at prior-year level, EBITDA before special items and core EPS to decline

The Bayer Group achieved its adjusted guidance for 2024. “We have three great businesses, with attractive long-term prospects,” CEO Bill Anderson said at the Financial News Conference on Wednesday. “However, to get to the opportunities ahead, we first need to steer through what will continue to be challenging times,” he noted, adding: “We still have work to do.” Anderson called 2025 a “pivotal year” for the company. It is the second year in Bayer’s turnaround and will be the most difficult in terms of financial performance, with net sales roughly in line with and earnings and free cash flow behind the prior year, he explained. The company expects improved performance from 2026 onwards. Alongside its four existing strategic priorities, the company is adding profitability at Crop Science as a fifth focus area, coupled with the launch of a comprehensive, five-year plan to improve earnings. “You’re going to see us with our sleeves rolled up, focused on taking the right actions to set up our customers, our company and our owners for a prosperous future,” he added.

In the Pharmaceuticals Division, for example, the company expects to increase the combined sales of the cancer drug Nubeqa™ and Kerendia™, for the treatment of chronic kidney disease associated with type 2 diabetes, from around 2 billion euros to more than 2.5 billion euros in 2025, Anderson said. This year, it is also planning to launch the heart drug Beyonttra™ (active ingredient: acoramidis) and elinzanetant, a non-hormonal treatment for menopause symptoms. The Pharmaceuticals Division is projected to return to sales growth from 2027 onwards and expand margins beginning in 2028, he added. Furthermore, the company remains active in its efforts to address the US litigations, both inside and outside the courtroom, with Anderson seeing tangible steps toward containment on the horizon this year. Bayer is committed to significantly containing the related risks by the end of 2026, he explained. In addition, the company remains focused on deleveraging and advancing Dynamic Shared Ownership, Anderson said. The new operating model is expected to deliver savings of 800 million euros for 2025, on top of the approximately 500 million euros in savings that were targeted and achieved in 2024, he added.

The plan to boost profitability at Crop Science centers around key measures regarding the product portfolio, research and development, production, commercial and enabling functions, totaling more than one billion euros in annual earnings contributions by 2029. It also includes a far-reaching cash productivity program. Bayer is targeting above-market growth for Crop Science during the coming years, with more than 3.5 billion euros of incremental sales from innovation by 2029. By the same year, the division is targeting an EBITDA margin before special items in the mid-20s percentage. “We recognize the need to take action, our team has a plan, and they’ve got what it takes to deliver,” Bill Anderson said.

Group sales at prior-year level, free cash flow slightly higher than projected

Group sales came in at 46.606 billion euros in 2024, up 0.7 percent on a currency- and portfolio-adjusted basis (Fx & portfolio adj.). There was a negative currency effect of 1.349 billion euros (2023: 1.964 billion euros). EBITDA before special items decreased by 13.5 percent to 10.123 billion euros. This figure included a negative currency effect of 573 million euros (2023: 375 million euros). EBIT amounted to minus 71 million euros (2023: plus 612 million euros) after net special charges of 5.507 billion euros (2023: 6.977 billion euros). The special charges mainly resulted from impairment losses, which were primarily attributable to the Crop Science Division. Net income came in at minus 2.552 billion euros (2023: minus 2.941 billion euros), while core earnings per share declined by 21.0 percent to 5.05 euros.

Free cash flow more than doubled against the prior year, rising to 3.107 billion euros and slightly exceeding the company’s expectations. Net financial debt amounted to 32.626 billion euros as of December 31, 2024, down 5.4 percent from year-end 2023. In order to further reduce debt and gain greater flexibility, the company intends to pay out the legal minimum in dividends for 2024, as previously announced. It is therefore proposing an unchanged dividend of 0.11 euros per share entitled to the dividend at the Annual Stockholders’ Meeting on April 25, 2025.

Crop Science impacted by lower prices in crop protection business

Sales at Crop Science decreased by 2.0 percent (Fx & portfolio adj.) to 22.259 billion euros. Business was primarily impacted by lower prices in the crop protection business driven by competitive pricing pressure. Lower volumes in seeds and traits due to lower planted area were offset by volume growth in crop protection. Sales in Latin America were down due to lower planted corn area and reduced crop protection prices. By contrast, North America delivered slightly higher sales driven by higher crop protection volumes and soybean planted area, partially offset by lower corn planted area.

EBITDA before special items at Crop Science decreased by 14.2 percent to 4.325 billion euros, mainly due to significant price declines in the crop protection business. Earnings were also impacted by higher provisions for the Group-wide short-term incentive (STI) program as well as inflationary cost increases, whereas the cost of goods sold improved due to efficiencies, especially for crop protection products. There was also a positive currency effect of 37 million euros (2023: 103 million euros). The EBITDA margin before special items declined by 2.3 percentage points to 19.4 percent.

New products drive sales growth at Pharmaceuticals

Sales of prescription medicines (Pharmaceuticals) rose by 3.3 percent (Fx & portfolio adj.) to 18.131 billion euros. The division’s new products achieved significant gains, with growth rates of 78.2 percent (Fx & portfolio adj.) for Nubeqa™ and 73.9 percent (Fx & portfolio adj.) for Kerendia™. It also posted continued sales growth for the ophthalmology drug Eylea™, with an increase of 5.1 percent (Fx & portfolio adj.), as well as in the Radiology business, largely driven by higher volumes and prices for CT Fluid Delivery and Ultravist™. In addition, sales of the pulmonary hypertension treatment Adempas™ rose by a substantial 10.5 percent (Fx & portfolio adj.), with particularly strong gains in the United States. These positive effects were partially offset by declines for Xarelto™ in particular, with sales of the oral anticoagulant falling 13.0 percent (Fx & portfolio adj.) due to patent expirations.

EBITDA before special items at Pharmaceuticals decreased by 9.0 percent to 4.722 billion euros, mainly due to a negative currency effect of 491 million euros (2023: 221 million euros). Earnings were also impacted by higher provisions for the STI program as well as shifts in the product mix, reflecting declines for Xarelto™ and higher sales for Nubeqa™ and Eylea™ in particular, as well as the related increase in license fees. However, Pharmaceuticals was able to partially offset these effects thanks to lower expenses for projects in advanced clinical development and decreased selling expenses for its more mature products, while simultaneously increasing investments in early-stage research as well as in cell and gene therapy and chemoproteomics technologies. The EBITDA margin before special items decreased by 2.7 percentage points to 26.0 percent.

Consumer Health registers growth (Fx & portfolio adj.) in almost all categories

Sales of self-care products (Consumer Health) rose by 1.9 percent (Fx & portfolio adj.) to 5.870 billion euros against a strong prior year, with gains in almost all categories. Sales growth was strongest at Dermatology, which saw a 9.7 percent increase (Fx & portfolio adj.) that was primarily driven by continued strong demand for Bepanthen™. Business was also up by a substantial 8.2 percent (Fx & portfolio adj.) at Digestive Health, partly thanks to a normalized supply situation. By contrast, the division registered considerable declines in the Allergy & Cold business against a strong prior year, with sales falling 11.5 percent (Fx & portfolio adj.) due to a weaker season and inventory optimization by customers in the United States.

EBITDA before special items at Consumer Health decreased by 3.2 percent to 1.366 billion euros, mainly due to a negative currency effect of 46 million euros (2023: 133 million euros). Thanks to its continuous cost and price management efforts, the division was able to offset an increase in the cost of goods sold and higher investments in marketing and developing products. The EBITDA margin before special items came in at 23.3 percent, down 0.1 percentage points.

Group outlook: 2025 sales roughly at prior-year level

On a currency-adjusted basis (i.e. based on the average monthly exchange rates in 2024), Bayer expects to generate sales of 45 billion to 47 billion euros in 2025. This corresponds to a change of minus 3 to plus 1 percent on a currency- and portfolio-adjusted basis. On a currency-adjusted basis, the company anticipates EBITDA before special items of 9.5 billion to 10.0 billion euros, core earnings per share of 4.50 to 5.00 euros, and free cash flow of 1.5 billion to 2.5 billion euros. Net financial debt as of year-end 2025 is expected to amount to 31.0 billion to 32.0 billion euros on a currency-adjusted basis.

Bayer has also prepared its guidance based on the closing exchange rates as of December 31, 2024, and the differences to the currency-adjusted forecast above are as follows: At Group level, it expects to post EBITDA before special items of 9.3 billion to 9.8 billion euros, core earnings per share of 4.25 to 4.75 euros, free cash flow of 1.3 billion to 2.3 billion euros, and net financial debt of 31.2 billion to 32.2 billion as of year-end 2025.

Sustainability: Top marks for climate and water efforts

Bayer once again made major progress in its sustainability endeavors in 2024. The company is well on track to achieve its three “100 million” targets by 2030, which involve supporting smallholder farmers and providing access to modern contraception as well as self-care products. As part of its Climate Transition and Transformation Plan, Bayer last year defined concrete targets and mapped out the measures it plans to take in order to achieve net zero emissions across its entire value chain by 2050. The Science Based Targets initiative recently confirmed the company’s targets for reducing greenhouse gas emissions and validated its path to net zero. As the most important step in this regard, Bayer will continue its efforts to switch to renewable sources to meet its power and energy needs. In 2024, the company entered into agreements to secure significant amounts of power from renewable energy sources.

Bayer’s sustainability targets and related commitments to supporting people and protecting the environment will continue to be an integral part of its Group strategy moving forward, with the Board of Management having reaffirmed the sustainability strategy at the end of last year. CDP, a prominent non-profit organization, has recognized the company’s efforts in this area, having awarded Bayer the highest score of A in the categories of water and climate.

Notes:

The following tables contain the key data for the Bayer Group and its divisions for the full year and the fourth quarter of 2024.

The complete Annual Report 2024 is available on the internet at: www.bayer.com/annualreport

The speech given by the Bayer Board of Management to the media will be available online from around 10 a.m. CET at: www.bayer.com/speeches

Find more information at www.bayer.com.

Bayer erreicht angepasste Prognose und geht Herausforderungen entschlossen an

- 2025 wird ein zentrales Jahr für den Turnaround – verbesserte Performance ab 2026 erwartet

- Umfassender Plan zur Steigerung der Profitabilität im Agrargeschäft

- Fortschritte bei strategischen Prioritäten

- Konzernumsatz 2024 bei 46,606 Milliarden Euro (wpb. plus 0,7 Prozent), negative Währungseinflüsse von 1,349 Milliarden Euro

- EBITDA vor Sondereinflüssen bei 10,123 Milliarden Euro (minus 13,5 Prozent)

- Bereinigtes Ergebnis je Aktie bei 5,05 Euro (minus 21,0 Prozent)

- Konzernergebnis bei minus 2,552 Milliarden Euro, Wertminderungen bei Crop Science

- Free Cash Flow auf 3,107 Milliarden Euro gestiegen, Nettofinanzverschuldung verbessert auf 32,626 Milliarden Euro

- Vorgeschlagene Dividende bei 0,11 Euro pro Aktie

- Ausblick 2025: Umsatz ungefähr auf Vorjahresniveau, EBITDA vor Sondereinflüssen und bereinigtes Ergebnis je Aktie rückläufig

Der Bayer-Konzern hat seine angepassten Ziele für das Geschäftsjahr 2024 erreicht. Der Vorstandsvorsitzende Bill Anderson betonte bei der Bilanz-Pressekonferenz am Mittwoch: „Wir haben drei großartige Geschäfte mit langfristig attraktiven Entwicklungsperspektiven. Um diese Potenziale zu heben, müssen wir aber weiterhin durch unverändert herausfordernde Rahmenbedingungen navigieren. Wir haben noch Arbeit vor uns.“ 2025 sieht Anderson als „ein zentrales Jahr“ für das Unternehmen. Es sei das zweite Jahr auf dem Weg zum Turnaround und werde mit Blick auf die finanzielle Performance das schwierigste – mit einem Umsatz ungefähr auf Vorjahresniveau und einem Ergebnis sowie einem Free Cash Flow darunter. Eine verbesserte Performance erwartet der Konzern ab 2026. Neben den vier bisherigen strategischen Prioritäten liegt nun auch ein Hauptaugenmerk auf Profitabilität im Agrargeschäft (Crop Science) – mit einem umfassenden Plan für die kommenden fünf Jahre, um das Ergebnis zu verbessern. „Wir krempeln die Ärmel hoch und bringen die richtigen Maßnahmen voran, von denen unsere Kunden, das Unternehmen und seine Eigentümer in Zukunft profitieren“, sagte der Vorstandsvorsitzende.

So solle sich 2025 bei der Division Pharmaceuticals der Umsatz mit dem Krebsmedikament Nubeqa™ und Kerendia™ zur Behandlung der chronischen Nierenerkrankung in Verbindung mit Typ-2-Diabetes von zusammen rund 2 Milliarden Euro auf mehr als 2,5 Milliarden Euro erhöhen. Außerdem ist die Markteinführung des Herzmedikaments Beyonttra™ (Wirkstoff: Acoramidis) geplant sowie die von Elinzanetant zur nicht-hormonellen Behandlung von Wechseljahresbeschwerden. Bayer wolle bei Pharmaceuticals von 2027 an wieder Wachstum beim Umsatz erzielen und von 2028 an auch bei der Marge, so Anderson. Bei den US-Rechtsstreitigkeiten laufen die Aktivitäten inner- und außerhalb der Gerichtssäle weiter, und der Vorstandsvorsitzende stellte für dieses Jahr spürbare Fortschritte Richtung Eindämmung in Aussicht. Eine erhebliche Eindämmung der Risiken wolle Bayer bis Ende 2026 erreichen. Auch fokussiere sich das Unternehmen weiterhin auf den Schuldenabbau und die weitere Implementierung des neuen Organisationsmodells. Dynamic Shared Ownership solle dieses Jahr Einsparungen von 800 Millionen Euro zusätzlich zu den rund 500 Millionen Euro bringen, die 2024 wie geplant erzielt wurden.

Mit dem Plan für Crop Science soll die Profitabilität der Division steigen – und zwar durch Maßnahmen bei Produktportfolio sowie Forschung und Entwicklung, Produktion, Vertrieb und globalen Funktionen. Deren Ergebnisbeiträge sollen sich bis 2029 auf mehr als eine Milliarde Euro jährlich summieren. Hinzu kommt ein weitreichendes Programm zur Steigerung der Cash-Produktivität. Darüber hinaus strebt Bayer während der kommenden Jahre ein über dem Markt liegendes Wachstum von Crop Science an – mit einer Umsatzsteigerung von mehr als 3,5 Milliarden Euro durch Innovationen bis 2029. Die EBITDA-Marge vor Sondereinflüssen soll dann im mittleren 20-Prozent-Bereich liegen. „Wir haben Handlungsbedarf erkannt, unser Team hat einen Plan, und es hat das Zeug dazu, ihn umzusetzen“, sagte Bill Anderson.

Konzernumsatz auf Vorjahresniveau, Free Cash Flow etwas höher als prognostiziert

Der Konzernumsatz lag im Geschäftsjahr 2024 bei 46,606 Milliarden Euro, währungs- und portfoliobereinigt (wpb.) ein Plus von 0,7 Prozent. Währungseffekte belasteten mit 1,349 (Vorjahr: 1,964) Milliarden Euro. Das EBITDA vor Sondereinflüssen sank um 13,5 Prozent auf 10,123 Milliarden Euro. Hierin enthalten waren Währungseffekte von minus 573 (Vorjahr: minus 375) Millionen Euro. Das EBIT lag bei minus 71 (Vorjahr: plus 612) Millionen Euro. Darin enthalten waren Sonderaufwendungen von per saldo 5,507 (Vorjahr: 6,977) Milliarden Euro. Diese resultierten hauptsächlich aus Wertminderungen im Wesentlichen innerhalb der Division Crop Science. Das Konzernergebnis belief sich auf minus 2,552 (Vorjahr: minus 2,941) Milliarden Euro. Das bereinigte Konzernergebnis je Aktie sank um 21,0 Prozent auf 5,05 Euro.

Der Free Cash Flow stieg auf 3,107 Milliarden Euro – das war etwas mehr als vom Unternehmen in Aussicht gestellt und entspricht mehr als einer Verdoppelung im Vergleich zum Vorjahr. Die Nettofinanzverschuldung zum 31. Dezember reduzierte sich gegenüber Ende 2023 um 5,4 Prozent auf 32,626 Milliarden Euro. Um die Schulden weiter zu senken und die Flexibilität zu steigern, wird sich der Dividendenvorschlag für die Hauptversammlung am 25. April 2025 – wie bereits im vergangenen Jahr kommuniziert – auf das gesetzlich geforderte Minimum beschränken: unverändert 0,11 Euro je dividendenberechtigter Aktie.

Crop Science: Niedrigere Preise im Pflanzenschutzgeschäft belasten

Bei Crop Science ging der Umsatz wpb. um 2,0 Prozent auf 22,259 Milliarden Euro zurück. Die Entwicklung war im Wesentlichen von niedrigeren Preisen im Pflanzenschutzgeschäft durch verstärkten Wettbewerbsdruck geprägt. Geringere Absatzmengen im Bereich Saatgut und Pflanzeneigenschaften aufgrund reduzierter Anbauflächen konnten durch Mengensteigerungen bei den Pflanzenschutzprodukten kompensiert werden. In Lateinamerika sank der Umsatz aufgrund von rückläufigen Anbauflächen für Maissaatgut und Preisrückgängen im Bereich Pflanzenschutz. Das Geschäft in Nordamerika legte dagegen leicht zu. Dort konnten höhere Absatzmengen im Bereich Pflanzenschutz und gestiegene Anbauflächen für Sojasaatgut die geringeren Anbauflächen für Maissaatgut überkompensieren.

Das EBITDA vor Sondereinflüssen von Crop Science sank um 14,2 Prozent auf 4,325 Milliarden Euro. Dies ist im Wesentlichen auf erhebliche Preisrückgänge im Pflanzenschutzgeschäft zurückzuführen. Zusätzlich belasteten insbesondere höhere Rückstellungen für das konzernweite Short-Term-Incentive(STI)-Programm sowie inflationsbedingt gestiegene Kosten das Ergebnis. Positiv wirkten sich insbesondere bei Pflanzenschutzprodukten niedrigere Herstellungskosten durch Effizienzmaßnahmen aus. Zudem waren positive Währungseffekte von 37 (Vorjahr: 103) Millionen Euro zu verzeichnen. Die EBITDA-Marge vor Sondereinflüssen sank um 2,3 Prozentpunkte auf 19,4 Prozent.

Pharmaceuticals steigert Umsatz dank neuer Produkte

Der Umsatz mit rezeptpflichtigen Medikamenten (Pharmaceuticals) erhöhte sich wpb. um 3,3 Prozent auf 18,131 Milliarden Euro. Signifikante Zuwächse erzielten die neuen Produkte, Nubeqa™ (wpb. 78,2 Prozent) und Kerendia™ (wpb. 73,9 Prozent). Zudem steigerte die Division den Umsatz mit dem Augenmedikament Eylea™ (wpb. um 5,1 Prozent) sowie im Bereich Radiologie weiter, insbesondere dank Volumen- und Preiserhöhungen mit CT Fluid Delivery und Ultravist™. Deutlich legte auch das Geschäft mit Adempas™ zur Behandlung von Lungenhochdruck zu (wpb. um 10,5 Prozent), das insbesondere in den USA wuchs. Gegenläufig wirkten vor allem Rückgänge (wpb. minus 13,0 Prozent) beim oralen Gerinnungshemmer Xarelto™ infolge von Patentabläufen.

Das EBITDA vor Sondereinflüssen von Pharmaceuticals ging um 9,0 Prozent auf 4,722 Milliarden Euro zurück. Das war maßgeblich auf Währungseinflüsse von minus 491 (Vorjahr: minus 221) Millionen Euro zurückzuführen. Ergebnismindernd wirkten auch höhere Rückstellungen für das STI-Programm sowie Verschiebungen im Produktmix, gekennzeichnet durch das rückläufige Geschäft mit Xarelto™ und Umsatzerhöhungen vor allem bei Nubeqa™ und Eylea™, und damit einhergehende höhere Lizenzgebühren. Teilweise kompensieren ließ sich das durch gesunkene Ausgaben für Projekte der späten klinischen Entwicklung sowie niedrigere Vertriebskosten für reifere Produkte – bei gleichzeitiger Erhöhung der Investitionen in die frühe Forschung, in die Zell- und Gentherapie- sowie Chemoproteomik-Technologien. Die EBITDA-Marge vor Sondereinflüssen sank um 2,7 Prozentpunkte auf 26,0 Prozent.

Consumer Health wächst wpb. in fast allen Kategorien

Bei den rezeptfreien Gesundheitsprodukten (Consumer Health) erhöhte sich der Umsatz gegenüber einem starken Vorjahr wpb. um 1,9 Prozent auf 5,870 Milliarden Euro – mit Zuwächsen in nahezu allen Kategorien. Besonders deutliche Umsatzsteigerungen gelangen bei Dermatologie (wpb. 9,7 Prozent), vor allem dank einer anhaltend hohen Nachfrage nach Bepanthen™, und bei Magen-Darm-Gesundheit (wpb. 8,2 Prozent), unter anderem infolge der normalisierten Liefersituation. Merkliche Rückgänge gegenüber einer starken Vorjahresentwicklung waren hingegen bei Allergie- und Erkältungsprodukten (wpb. minus 11,5 Prozent) zu verzeichnen – aufgrund einer schwächeren Saison sowie der Bestandsoptimierung bei Kunden in den USA.

Das EBITDA vor Sondereinflüssen von Consumer Health sank um 3,2 Prozent auf 1,366 Milliarden Euro, vor allem aufgrund von Währungseinflüssen von minus 46 (Vorjahr: minus 133) Millionen Euro. Gestiegene Herstellungskosten und höhere Investitionen in die Produktvermarktung und -entwicklung konnten durch kontinuierliches Kosten- und Preismanagement kompensiert werden. Die EBITDA-Marge vor Sondereinflüssen reduzierte sich um 0,1 Prozentpunkte auf 23,3 Prozent.

Konzernausblick: Umsatz 2025 ungefähr auf Vorjahresniveau

Bereinigt um Währungseffekte (also auf Basis der monatlichen Durchschnittskurse des Jahres 2024) erwartet Bayer für das Jahr 2025 einen Umsatz von 45 Milliarden bis 47 Milliarden Euro. Das entspricht einer Veränderung von wpb. minus 3 bis plus 1 Prozent. Das Unternehmen rechnet mit einem EBITDA vor Sondereinflüssen von währungsbereinigt (wb.) 9,5 Milliarden bis 10,0 Milliarden Euro. Für das bereinigte Ergebnis je Aktie plant es wb. einen Wert von 4,50 bis 5,00 Euro. Der Free Cash Flow soll sich wb. auf 1,5 Milliarden bis 2,5 Milliarden Euro belaufen. Zum Jahresende 2025 rechnet der Konzern mit einer Nettofinanzverschuldung von wb. 31,0 Milliarden bis 32,0 Milliarden Euro.

Basierend auf den Wechselkursen zum Stichtag 31. Dezember 2024 rechnet Bayer abweichend von den oben genannten währungsbereinigten Werten auf Konzernebene mit einem EBITDA vor Sondereinflüssen von 9,3 Milliarden bis 9,8 Milliarden Euro, einem bereinigten Ergebnis je Aktie von 4,25 bis 4,75 Euro, einem Free Cash Flow von 1,3 Milliarden bis 2,3 Milliarden Euro und zum Jahresende 2025 mit einer Nettofinanzverschuldung von 31,2 Milliarden bis 32,2 Milliarden Euro.

Nachhaltigkeit: Bestnote für Engagement im Bereich Klima und Wasser

Im Bereich Nachhaltigkeit ist Bayer 2024 erneut wichtige Schritte vorangekommen und auf einem guten Weg, bis 2030 seine drei 100-Millionen-Ziele in den Bereichen Kleinbauern, moderne Verhütung und Zugang zu Self-Care-Produkten zu erreichen. Mit dem „Climate Transition und Transformation Plan“ hat das Unternehmen im vergangenen Jahr konkrete Ziele und Maßnahmen definiert, um bis 2050 über die gesamte Wertschöpfungskette hinweg Netto-Null-Treibhausgas-Emissionen zu erreichen. Die Science Based Targets Initiative hat jüngst die Ziele von Bayer zur Reduktion von Treibhausgasemissionen bestätigt und den Weg hin zu Netto-Null validiert. Die wichtigste Maßnahme in diesem Zusammenhang wird auch künftig die weitere Umstellung zur Nutzung von Strom und anderen Energieträgern auf Basis erneuerbarer Energien darstellen. Im Jahr 2024 hat Bayer Verträge zur Lieferung von Strom aus erneuerbaren Energien in bedeutendem Umfang abgeschlossen.

Die Nachhaltigkeitsziele und das damit verbundene Engagement für Mensch und Natur sind auch in Zukunft fester Bestanteil der Konzernstrategie von Bayer. Dies hat der Vorstand durch Bestätigung der Nachhaltigkeitsstrategie Ende vergangenen Jahres unterstrichen. Die bekannte Non-Profit-Organisation CDP hat das Engagement des Unternehmens mit der Bestnote A in den Bereichen Wasser und Klima anerkannt.

Hinweise:

Die folgenden Tabellen zeigen Kennzahlen des Bayer-Konzerns und seiner Divisionen zum Gesamtjahr sowie zum 4. Quartal 2024.

Der vollständige Geschäftsbericht 2024 ist im Internet verfügbar unter www.bayer.com/de/geschaeftsbericht

Die Presse-Rede des Bayer-Vorstands ist ab ca. 10 Uhr MEZ im Internet verfügbar unter: www.bayer.com/de/reden

Mehr Informationen finden Sie unter www.bayer.com/de.